There is no law requiring local governments to provide fire protection services to residents. But even in small towns like Creston, residents have come to take them for granted.

Creston’s town councillors learned that providing fire protection is optional during a Jan. 6 presentation by Creston Fire Rescue Chief Mike Moore. Perhaps more importantly, considering that abolishing the fire department would not likely be tolerated by taxpayers, they also learned that their decisions have a direct impact on insurance rates for residences and businesses.

“Insurance against fire damage is complicated, but rates are tied to the level of fire protection a community can offer, as well as the risks associated with the type of construction and industry,” Moore said.

In an information package distributed to councillors, a brief explanation of the Fire Underwriters Survey was included.

“Qualified surveyors conduct full field surveys of the fire risks and defenses in municipalities and built-up communities across Canada and the results of these surveys are used to establish the Public Fire Protection Classification (PFPC) of all communities,” according to the FUS. “While the survey is not involved in rate-making matters, the information is one of several factors used in the development of property insurance rates, particularly those applying to commercial, industrial, multi-family and institutional occupancies.”

Insurance companies assess, with the help of tools like the FUS, fire risks in communities. Fires in single dwellings are less likely to spread to other properties, for instance, than those in apartments or the downtown core, where buildings as much as a century old connect with neighbouring properties.

“In the event of a fire downtown it is entirely possible that I will have to make a decision about whether to call in excavators to raze perfectly good buildings in order to save an entire block — or blocks — from going up in flames,” Moore said.

In addition to assessing fire hazards, insurance companies also factor in the ability of fire departments to contain and minimize damage.

Among the many considerations are equipment, number of full-time (career) fighters, number of volunteers and their training and availability, and, of course, the distance that buildings are from fire halls and water supplies.

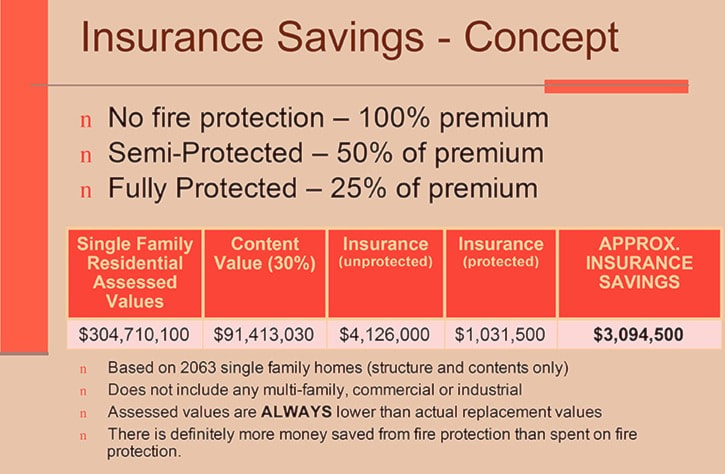

Calculations are complex, but certain guidelines serve as indicators of how insurance rates will be affected by adding or reducing service levels.

If a community works to reduce fire risks and improve firefighting levels, more insurers can serve the area. Increasing competition results in more choice and lower rates. Individual companies can only provide so much insurance coverage in a specified area so that their overall exposure is limited in the event of large fire losses. Lower risks and higher fire protection capability increase the amount of coverage any company can take on, and increase the number of companies that can compete in the area.

According to the FUS, “Property owners can receive significant cost savings on insurance rates when the fire insurance grade in a community improves. For example, compare an attached dwelling property insured in a community with no fire protection recognized by fire insurance grading as to a property with identical characteristics in a community with a fire insurance grade that correlates to ‘protected’. The difference in fire insurance rates could be as much as 70 per cent per year. If the base cost of insurance is $2,000 a year, and when considered across hundreds of similar properties, the cost benefit of providing fire protection services that are recognized for fire insurance grading purposes is readily apparent.”

Moore cautioned councillors that not all improvements to local fire service are significant enough to influence insurance rates.

“The cost-benefit consideration is always going to be an important part of your decision-making process,” he said.

This is the second in a series about fire service in Creston. Last week’s installment focused on the amount of local calls and potential financial impact.

Next week: Meet the five work experience firefighters who are living in Creston for a year.